New ATO guidance on personal services income is putting profit-splitting arrangements under the microscope — here's what business owners need to check before 30 June 2027.

If you run your business through a company or trust, this one's for you.

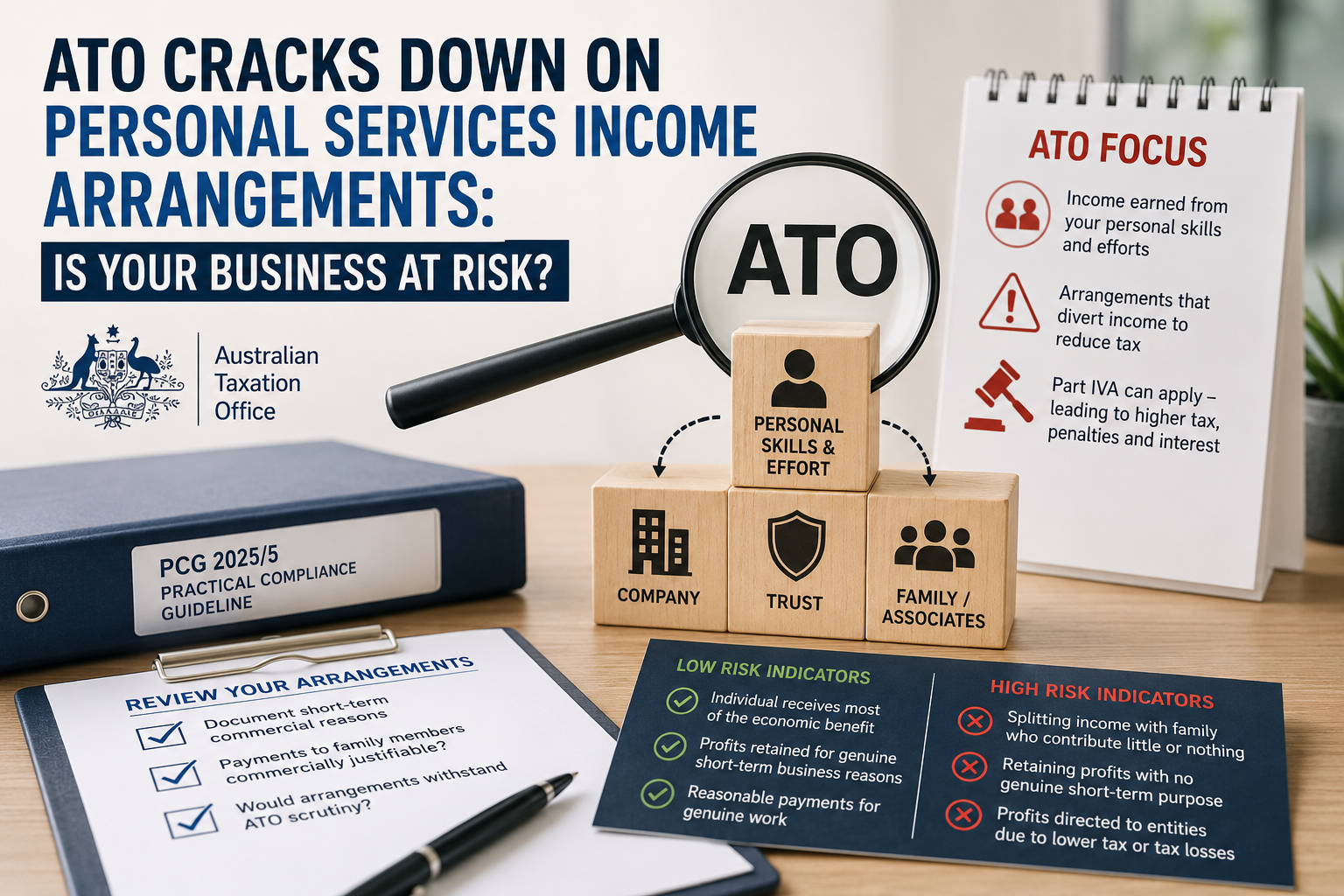

The ATO has just released new guidance — PCG 2025/5 — that spells out exactly how it plans to treat income earned from your personal skills and effort when that income gets routed through a company or trust structure. Assistant Commissioner Tony Poulakis flagged the update recently, and it's worth taking seriously.

Why this matters to you

Plenty of business owners operate through a company or trust for good reasons — asset protection, flexibility, succession planning. Nothing wrong with that. But when most of the income is really coming from you — your skills, your effort, your reputation — and the structure is being used to shift that income to someone (or something) taxed at a lower rate, the ATO calls that "alienation" of personal services income, and it's squarely in their sights.

Here's the part that catches people out: even if your business technically passes the tests to be classified as a Personal Services Business, that doesn't automatically protect you. The ATO can still apply the general anti-avoidance rules under Part IVA if the arrangement looks like it was mainly set up to save tax. And if Part IVA bites, you're looking at back tax, penalties, and interest.

What the ATO sees as reasonable

The core question is simple: is the person actually doing the work getting a fair share of the profit? Arrangements tend to sit in the "low risk" zone when:

- The person doing the work is paid appropriately through salary, wages, director fees, bonuses, or trust distributions

- Any profit kept back in the company has a genuine, short-term business purpose — think funding an equipment purchase, backed by an actual plan that gets followed through

- Family members or associates are only paid for real work they've actually done, at a reasonable rate

What will get you noticed

On the flip side, the ATO has been upfront about what raises flags:

- Splitting income with family who've contributed little or nothing to earning it

- Leaving large profits sitting in the company with no genuine short-term reason

- Directing profits toward entities or people mainly because they're taxed more favourably or have losses to soak them up

Put simply — the bigger the gap between who did the work and who ends up paying tax on it, the more attention your structure is likely to attract.

A window to get things right

There's some good news here. The ATO has given businesses a transition period: if you genuinely review your arrangements and move from higher-risk to lower-risk by 30 June 2027, you're unlikely to face Part IVA action on the arrangements you've corrected. It's not a free pass — but it is a real chance to get ahead of it.

What you should do now

This is a good moment to sit down and look honestly at how profit flows through your structure. Ask yourself:

- Can I actually justify, on paper, why profit is being retained in the company?

- Are payments to family members genuinely tied to work they've done?

- If the ATO reviewed this tomorrow, would it hold up?

If you're earning income mainly from your own skills and effort and running it through a company or trust, don't wait for a review letter to find out where you stand. A proactive conversation now is a lot cheaper than an ATO audit later.

Want us to take a look at your structure before 30 June 2027? Get in touch — this is exactly the kind of thing we help clients get right.

Need Help with your Business, Bookkeeping, Tax or SMSF requirements?

If you would like a little help, please get in touch with us for assistance. We can help with your business, bookkeeping, tax and SMSF requirements. To book an appointment, use our online booking system, give us a call on 07 3289 1700, or email us at reception@rgaaccounting.com.au.We look forward to assisting you this tax season!

Please also note that many of the comments in this publication are general in nature and anyone intending to apply the information to practical circumstances should seek professional advice to independently verify their interpretation and the information’s applicability to their particular circumstances. Should you have any further questions, please get in touch with us for assistance with your SMSF, business, bookkeeping and tax requirements. All rights reserved. Brought to you by RGA Business and Tax Accountants. Liability Limited by a scheme approved under Professional Standards Legislation.